What Is Professional Indemnity Insurance And How Does It Work?

Enterprises constantly need to think a step ahead and thwart an unforeseen consequence even before it takes place. Despite exercising extreme caution, businesses could still quite possibly leave room for error at times. The price for even a slight overlook could be a bottomless pit of legal and other associated expenses. This is where professional indemnity insurance comes in.

Professional indemnity insurance is designed to take care of risks associated with professional liability. A professional indemnity insurance policy primarily caters to professionals or organizations to help manage their risks, especially the ones pertaining to their clients.

In today’s high-risk climate, this policy finds a rapidly growing relevance for organizations to navigate through civil liability and prevent any large expenses that may follow with such risks. Here’s all that you need to know about professional indemnity insurance and why it is a prudent business investment in today’s times.

What is Professional Indemnity Insurance?

Professional indemnity insurance is a type of insurance policy that is developed especially for a business providing professional services or consultations to its clients. Given the growing focus on responsibility and answerability in today’s corporate atmosphere, including extensive professional liability insurance is a crucial element of any risk management programme.

Essentially it entails that if there’s an alleged failure or negligence in the delivery of any of these services, organizations shall be liable to pay their clients for the losses incurred. Additionally, they may also be held legally liable for these risks and losses. The compensation for these risks can run significantly high, thereby bleeding a business dry even with one single case. The organizations, therefore, need to cover themselves way ahead of any such occurrence.

Professional indemnity insurance comes to their rescue in this case, compensating them for costs that may occur as a result of lawsuits from their clients.

Who Should Opt for Professional Indemnity Insurance?

Ideally, the professional indemnity cover is meant for any business dealing with clients. But practically, it is a protective shield for both businesses as well as professionals. Traditionally, the term “professionals” would translate to roles like accountants, engineers or lawyers. However, that has largely changed with the times and now, the term has taken a much broader meaning and extends to any person who provides any kind of consultancy or services in a professional capacity.

Therefore, any business that deals directly with clients for providing any kind of consultation or service should definitely opt for this policy in order to protect themselves from any possible legal claims raised by the client in the future.

While professional indemnity insurance is essentially a legal liability cover, it also covers other related expenses that the insured may incur in the course of their defense. These could also include damages or losses awarded to the third party.

The policy could be bought by a range of professionals, including but not limited to accountants, construction engineers, architects, interior designers, marketing and media professionals, and travel agents among many others. Opting for the right insurance policy not only shields one against civil liability but also financial and reputational loss.

Why is Professional Indemnity Insurance Needed?

We live in an era of growing financial literacy and awareness where clients are much more cognizant of risks before they enter into a contract with the company. While it is arguable that one may have an agreeable working relationship with their clients, this still is no guarantee of preventing future litigations from their end.

Depending on the nature of the lawsuit, the legal battle could sometimes persist for years. Even one such incident is enough to liquidate the financial foundation of an enterprise, irrespective of how small or large it may be. This is especially all the more relevant for businesses that serve high-value clients, as the stakes are higher in this case.

Apart from this, the dealing by several organizations is not just limited to domestic clients, but also extends to serving customers overseas. In this case, the business dealing with litigious countries should certainly go for a higher cover amount.

In fact, having a standardized professional indemnity cover is often imposed as a mandatory requirement for signing a contract overseas. As clients become more aware of their legal rights to hold professionals or businesses liable for their financial loss, the need for professional indemnity cover is transforming into an indispensable part of business operations and risk management strategy.

What are the Risks Covered Under Professional Indemnity Insurance?

The concept of professional indemnity insurance is fundamentally based on compensating the insured party against the risk of being exposed to civil liability. Here are the primary risks that are covered by a professional indemnity policy –

- Breach of confidentiality

The policy offers coverage to the insured against intentional or unintentional disclosure of information resulting in financial loss to a company. - Infringement of intellectual property

It also covers the legal costs or legal defense costs associated with pursuing infringement or theft of intellectual property or copyright. - Impaired or unauthorized access

The damages that occur due to unauthorized access and losses arising due to the same are covered under this policy. - Civil fines and penalties

Due to any negligence, the civil fines and penalties imposed on the insured party shall be covered by the insurance company. - Libel, slander and defamation

It includes coverage for defamatory statements or materials which can have a negative impact on the reputation of a person in the eyes of others. - Breach and delay in duty

The policy covers damages caused due to delays in the execution of services that the client may face. In addition, it provides coverage against the bad faith of employees in case of any breach of duty. - Disputed Fees

It includes claims made against professionals arising from a disagreement about the fees charged by such professionals.

General Exclusions under Professional Indemnity Insurance

- Wilful negligence or misconduct

No insurance policy can safeguard an individual or business from intentional damage. Like all the other policies, PI policy also works on utmost good faith and therefore, no wilful negligence or misconduct shall be compensated for by the insurer. - Liability arising from illegal violations

The insurance ecosystem is bound to follow the law of the land and can only cover a party within the legal boundaries. So, if the insured is held liable for an illegal violation committed by them in a professional capacity, the professional indemnity policy or its features will not get triggered. - Claims before buying the policy

Any existing claims before the policy is bought shall not be entertained by the insurer under any circumstances. The insurance is only meant to cater to the future possibility of claims, and so the coverage starts only from the day the policy is bought. - Alcohol or drug influence

While professional indemnity cover is supposed to take care of professional negligence, it does not factor in the effect of alcohol or drugs while discharging the duties. Therefore, if negligence occurs due to or under drug or alcohol influence, the insurer will reject your claim. - Nuclear or war-related perils

Like most policies,perils pertaining to nuclear or war situations are not covered by the professional indemnity cover as well. The policy will only cover losses incurred in a professional capacity by the insured.

Factors to Consider Before Choosing Professional Indemnity Insurance

- Deciding the right sum insured

Sum insured is the most crucial part of any policy, so one should decide an adequate amount that will cover them sufficiently in case a claim arises. Unlike the popular notion, the sum insured is not dependent on the service or consultation fee charged, rather, it is decided by the nature and magnitude of risks that a particular business carries. - Full disclosure of information

Never hide any piece of information from your insurer at the time of issuance of the policy. This could defeat the entire purpose of buying the insurance in the first place as the insurer is entitled to reject your claim on the grounds of incomplete disclosure. No matter how small or insignificant, every bit of information should be detailed out.

- Note the deductibles and sub-limits

The nature of risk differs with every business and so does the premium. Some popular ways to bring down your premium are – opting for plans that have deductibles or sub-limits. While this will lower your premium, opting for a deductible will require you to shell out some part of the payment out of your own pocket at the time of claim settlement. Similarly, plans with sub-limits come with a lower premium but can restrict your coverage at the time of claim. So, choose accordingly. - Aligning policy features with business needs

It is of utmost importance to align your business needs with the features you opt for in your policy. For instance, if your business primarily deals with clients overseas, you should steer clear of policies offering only domestic coverage and instead, buy a policy that covers you outside the country’s boundaries.

Also, you should assess the nature of the risks that your business carries. Considering that the risks of a marketing enterprise will substantially differ from the risks of a construction business, the policyholders should be mindful of the kind of coverage they are opting for.

Lastly, do not forget to compare the features online and choose what suits the needs of your business the best. Always remember to thoroughly comb through the fine print and check with your insurer regarding any doubts that you might have.

Professional indemnity insurance: What is it and how does it work?

All your professional indemnity questions answered

Mistakes are an inevitable part of any business. These lapses, however, can result in huge financial losses and reputational damage, particularly if a client decides to sue. This is where professional indemnity insurance comes into play. Although not always legally required, this type of coverage is crucial for many businesses, especially for those that provide expert or advisory services.

This article discusses how professional indemnity insurance works in different occupations and why in most industries it is considered an essential form of financial protection. We encourage insurance agents and brokers to share this guide with their clients to help them find the coverage that best fits their businesses’ needs.

What is professional indemnity insurance?

Professional indemnity (PI) coverage is a type of business insurance policy that protects companies against claims of financial losses resulting from alleged or actual negligence during the fulfilment of a professional service. Depending on the industry, this form of protection can be referred to by different names – for example, errors and omissions (E&O) insurance in real estate, professional liability insurance (PLI) in construction, or malpractice insurance in the medical and legal fields.

According to the Insurance Information Institute (Triple-I), professional indemnity insurance policies come in two types:

- Claims-made policies: Cover claims only if the error was committed and the lawsuit was filed when the policy was in effect.

- Occurrence policies: Cover any claims that have taken place during the coverage period, even if the charges were filed after the policy lapses.

What is the purpose of professional indemnity insurance?

Regardless of the industry, each professional needs to perform their jobs without the fear of unintended consequences. This is the purpose of professional indemnity insurance. This type of coverage allows professionals to act in the best interests of their clients and businesses knowing they are protected in the event they make a mistake.

PI insurance varies from other forms of liability coverage – general liability insurance and product liability insurance.

General liability insurance, sometimes referred to as business liability or public liability coverage, protects companies against claims of bodily injury or property damage resulting from their business activities. Businesses also do not receive compensation for this type of coverage. Instead, the payouts are given to the affected third party. Without this type of protection, companies will need to pay for the claims out of pocket.

Product liability coverage protects businesses against lawsuits from customers claiming losses or injury because of their products. Designed for companies that sell products, this form of insurance policy also covers legal defence costs and compensation if the business is found to be at fault.

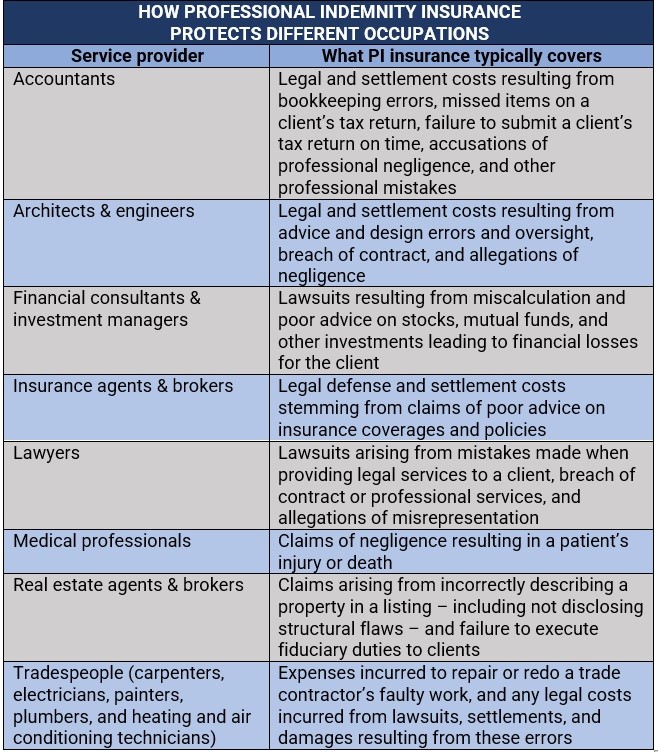

What does professional indemnity insurance cover?

A professional indemnity insurance policy covers legal and settlement costs arising from service-related mistakes. These include:

Professional negligence

This happens when a professional fails to perform their duties and obligations to a required standard. Some instances where professional negligence occurs include an accountant giving poor financial advice, causing a client to miss out on huge tax benefits and a medical professional administering the wrong medication, resulting in severe complications, or the death of, a patient.

Breach of contract

This occurs when a professional breaks the agreed-upon terms and conditions of a binding contract. This includes failure to deliver a specific service stated in the contract, resulting in huge financial losses for a client.

Misrepresentation

This happens when a professional makes a false statement that causes a customer to agree to a contract. This can include real estate agents padding the square footage of a property to raise the property’s value or an insurance professional inflating service costs or charging for services that were not rendered. If misrepresentation is discovered, the affected party can void the contract and seek damages.

Professional misconduct

This occurs when a professional violates the rules or standards set by their profession’s legal body. This includes:

- Failure to get a client’s informed consent

- Withholding important information to clients

- Working while impaired

- Breach of confidentiality

- Inadequate documentation and record keeping

What does professional liability insurance exclude?

Professional liability policies do not cover:

- Legal or medical expenses resulting from bodily injury.

- Property damage that customers suffer while a service is being provided.

- Lawsuits filed by employees due to accusations of wrongful termination or workplace harassment.

The first two are covered by general liability insurance, the third is covered by employment practices liability coverage.

Why do I need professional indemnity insurance?

Any individual or business that offers professional services or advice to clients should take out professional liability coverage – and for good reason. Allegations of negligence, inaccurate advice, and misrepresentation can result in exorbitant costs that can easily drain a company’s financial resources, whether they are proven liable or not. Professional indemnity coverage can protect them financially from the huge expenses arising from lawsuits.

The table below sums up how professional indemnity insurance protects certain occupations.

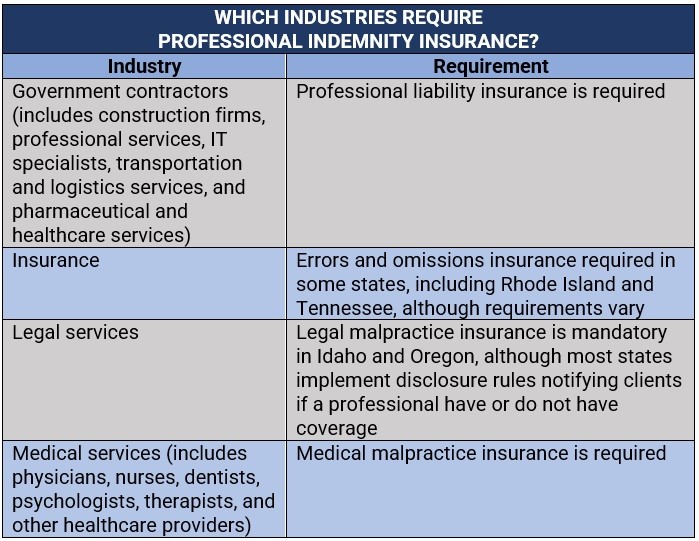

When is professional indemnity insurance required?

Businesses in certain industries are required, either by law or industry standards, to take out professional liability insurance. Some clients may also require a professional or a company to have this type of coverage in place before agreeing to do business. These are some of the professions where coverage is necessary in the US:

Medical practitioners

Medical professionals are required by law to carry medical malpractice insurance. These include:

- Doctors and physicians

- Nurses

- Dentists

- Psychologists

- Occupational, physical, and speech therapists

- Other healthcare providers

This type of professional indemnity insurance protects practitioners in the medical field against claims of negligence resulting in a patient’s injury or death.

Lawyers

Currently, legal malpractice insurance is mandatory only in two states – Idaho and Oregon. Nearly half of all US states, however, have implemented some form of disclosure rules requiring lawyers to notify clients whether or not they carry coverage.

Real estate professionals

Taking out errors and omissions insurance is compulsory for real estate agents and brokers in several states. These include:

- Colorado

- Idaho

- Iowa

- Kentucky

- Mississippi

- Nebraska

- New Mexico

- North Dakota

- Rhode Island

- South Dakota

- Tennessee

- Wyoming

Requirements, however, vary between states. In Colorado and Nebraska, for instance, real estate agents are required to get a policy with a minimum annual aggregate limit of $300,000. In Iowa and Mississippi, meanwhile, the minimum limit is $100,000.

Insurance professionals

Several states also require insurance agents and brokers to carry errors and omissions coverage. Similar to those for real estate professionals, each state has a different set of requirements. In Rhode Island, industry professionals need to have coverage with a minimum aggregate policy limit of $500,000. In Tennessee, the minimum limit is $100,000.

Government contractors

Under the Federal Acquisition Regulation (FAR), businesses working on government projects are required to carry professional liability insurance to protect them from “the perils to which the contractor is exposed.” These businesses include:

- Construction firms

- Professional services providers, including financial and public relations firms

- IT specialists, including consultants and cybersecurity experts

- Transportation and logistics services providers

- Pharmaceutical and healthcare services providers

Whether professional indemnity insurance is mandatory for a certain occupation also depends on the region. Professionals in Canada and the UK are not required by the law to take out insurance, although several industry bodies make coverage compulsory for individuals and businesses to operate. In Australia, PI insurance is required for occupations considered high-risk, including:

- Accountants

- Architects

- Bookkeepers

- Engineers

- Legal practitioners

- Healthcare professionals

- IT consultants

- Marketing consultants

- Real estate professionals

Is professional indemnity insurance compulsory?

Not all occupations are legally required to take out professional indemnity insurance. But even if coverage is not always compulsory, industry experts advise most individuals and companies to purchase this type of financial protection, especially if they are in the business of providing expert or advisory services.

Here are some occupations where professional indemnity insurance is considered essential.

List of industries where professional indemnity insurance is compulsory

As mentioned in the previous sections, not all occupations are required by the law to secure professional liability insurance. However, some industry associations make it compulsory for professionals in their field to take out coverage for them to practice or operate their businesses.

Here’s a summary of the industries where professional indemnity insurance is mandatory in the US.

What is another name for professional indemnity insurance?

Professional indemnity insurance is also called professional liability insurance. It provides compensation against damages caused by mistakes made by a company or a professional while working.

Occasionally, professional indemnity insurance is also known as errors and omissions (E&O) insurance. The cover will be indemnity against claims arising out of errors and omissions in the policyholders’ professional service.

Professional indemnity insurance can help protect businesses and professionals from these types of claims:

- Negligence

- Breach of contract

- Misrepresentation

- Fraud

- Defamation

An insurance company would usually take care of the expenses incurred during the defense against such a suit and the amount compensated in favor of the plaintiff.

Businesses and professionals often depend on professional indemnity insurance to protect them from any unforeseen financial losses. This becomes crucial for small business owners and even professionals who cannot afford the huge costs incurred by such a lawsuit.

Here are other points to consider about professional indemnity insurance:

- The cost of professional indemnity insurance varies depending on the type of business or profession, the level of coverage desired, and the size of the business or profession.

- Professional indemnity insurance is typically purchased on an annual basis.

- Most professional indemnity insurance policies have an insurance deductible

- Professional indemnity insurance policies typically have a limit of liability, which is the maximum amount that the insurance company will pay for covered claims.

If you are a business owner or professional, it is important to consider purchasing professional indemnity insurance. It can help protect you from financial losses resulting from claims of negligence, errors, or omissions in your work.

Who should have professional indemnity?

Professional indemnity insurance covers professionals offering guidance and service to other people. This includes professionals such as:

- Accountants

- Lawyers

- Doctors

- Engineers

- Architects

- Consultants

- Real estate agents

- Insurance agents

- Financial advisors

Professional indemnity insurance guarantees compensation against financial losses arising from allegations of malpractice, errors, oversight, or other omissions.

Here are some specific examples of situations where professional indemnity insurance can be helpful:

- The client is overcharged by the IRS and pays additional taxes and penalties due an oversight of an accountant

- A lawyer’s error causes his client to lose the case

- The patient is injured because the doctor made a mistake during treatment

- The client loses money on account of the bad advice from a consultant

- A client loses money due to bad investment advice given by a financial advisor

What does professional indemnity not cover?

Professional indemnity insurance is comprehensive in its coverage, yet it doesn’t cover everything. Here are some of the most common exclusions:

- Intentional wrongdoing: professional indemnity insurance does not cover claims of intentional acts of wrongdoing like fraud, dishonesty, and criminal behavior.

- Pre-existing conditions: Claims arising from losses suffered before professional indemnity insurance was taken out are not covered.

- Fines and penalties: Penalties and fines, imposed by regulatory bodies, for example, are not covered by professional indemnity insurance.

- Bodily injury and property damage: Professional indemnity insurance does not cover bodily injury and property damage, but general liability insurance would usually cover these.

- Disputes with employees: Professional indemnity will not cover disputes between a professional and an employee, like a claim for unlawful dismissal or discrimination.

- Contractual disputes: Contract disputes between professionals and their clients are not covered by professional indemnity insurance.

It is crucial to go through your professional indemnity insurance policy to understand what is included. For any questions, talk to your agent/broker.

Professional indemnity insurance should not be treated as a substitute for good professional practice. A professional should always aim for good quality services, take precautions not to make simple errors.

While professional indemnity insurance might be of little help if an error happens, it will make up for this with adequate compensation.

What experiences do you have with professional indemnity insurance? Let us know in the comments section below.

Why Indemnity and Liability Insurance are important

If you own a business, you may become liable for damages to another property or person caused by your business. You could also face claims of negligence or breach of duty in providing a professional service or advice.

The threat of potential claims and litigation is very real in today’s business environment and can potentially bankrupt businesses, small or large.

You may think “it will never happen to me”, but legal action often comes from an unforseen event.

Liability and indemnity are two types of insurance that protect your business against legal claims. Making sure you have the right cover for liability and indemnity is vital to your business.

Public Liability Insurance protects you and your business against the financial risk of being found liable for personal injury, property damage and economic loss.

Professional Indemnity Insurance protects you and your business against claims for alleged negligence or breach of duty arising from an act, error or omission in the performance of professional services.

The cost of litigation

Many businesses underestimate the real cost of legal action. The cost for a defence could be around the $100,000 mark. Many businesses – especially small businesses – would struggle to fund these costs.

For example, a case handled by CGU saw a professional involved in a lawsuit that extended to $1 million in legal fees alone over several years.

His insurance premium covered all associated costs and the case was handled by the company. More importantly, he was proven not to have been negligent.

Protecting your professional reputation

This illustrates an important factor in professional indemnity – the often overlooked issue of reputation defence.

There can be a tendency in such legal cases for the professional involved to try to settle the case as quickly as possible.

While it may seem like the easiest solution, it’s important to consider the long-term impact. It can be seen as an admission of guilt, and have a devastating effect on your reputation.

Professional Indemnity Insurance enables you to pursue legal avenues to clear your name and defend your reputation – with the backing of a legal and insurance team.

When advice is your livelihood, the right professional indemnity cover can offer peace of mind, security and most importantly, protect your valuable reputation.